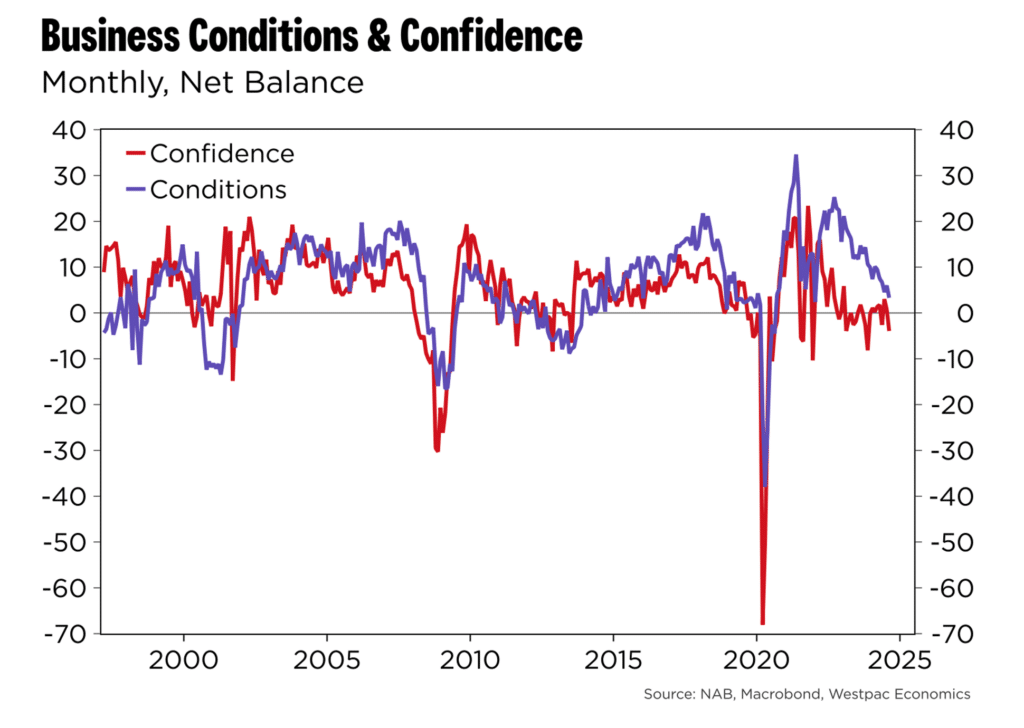

October brought mixed signals for Australia’s economy — and a growing dilemma for the Reserve Bank.

The RBA held rates steady at its latest meeting, citing elevated inflation and

Specialist real estate private credit investment manager, Zagga, has secured $65 million through an oversubscribed corporate note arranged by fixed income specialist, FIIG Securities.

The four-year, senior secured note

STOCKHEAD & THE AUSTRALIAN

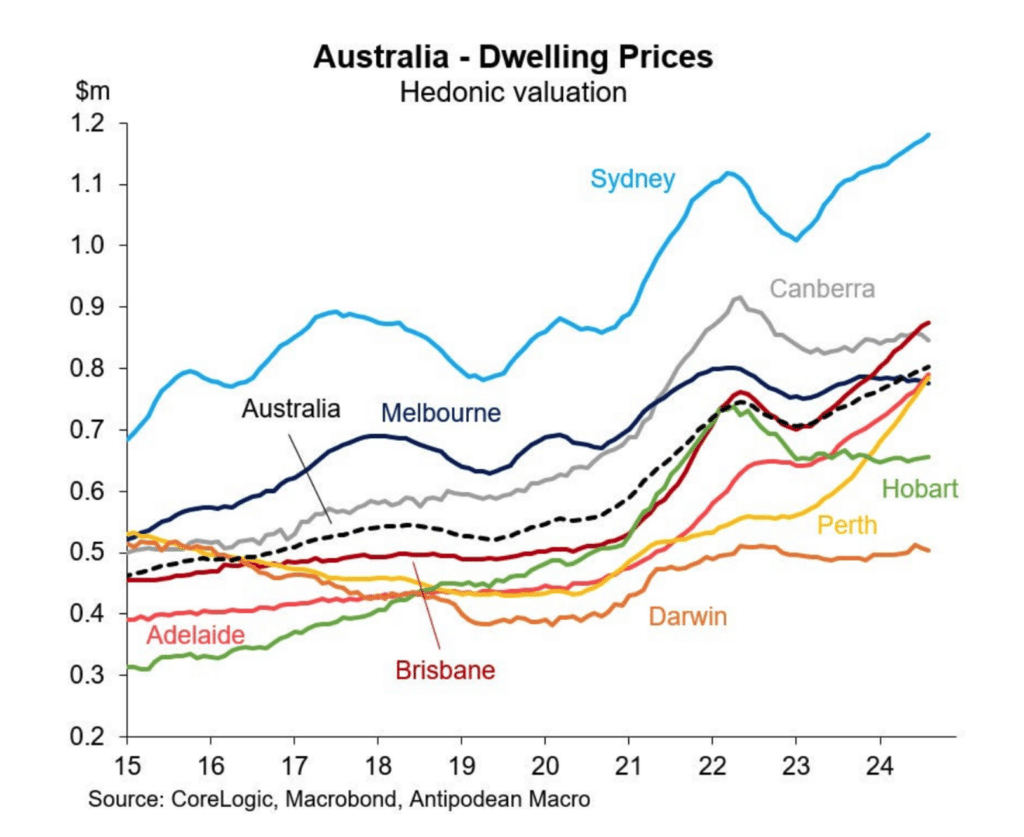

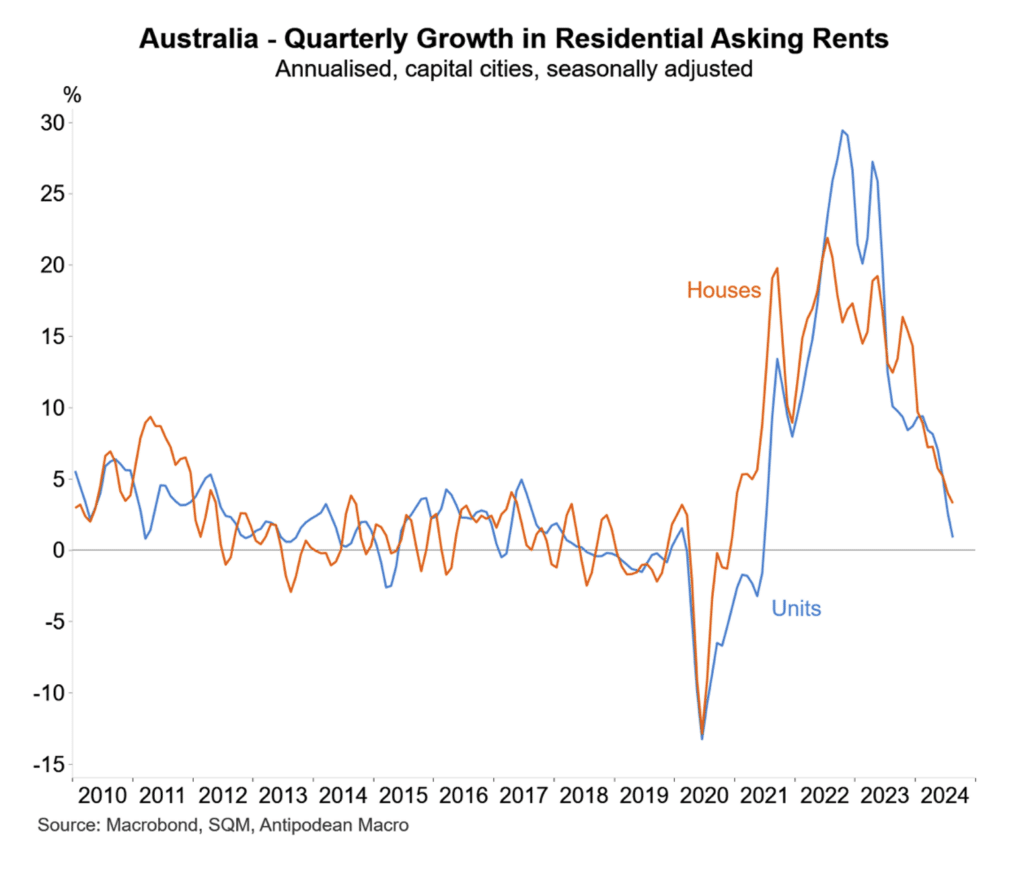

Australia’s favourite asset isn’t listed on the ASX. It’s the thing people live in, argue over at auctions, and quietly trust as their financial foundation