In today's multifaceted investment landscape, sophisticated investors are seeking alternative investment opportunities which provide a more attractive return for risk proposition with lower volatility than what is currently available in the public markets.

Among the various options available, “first mortgage investments”, as a subset of alternative real estate investments, have gained significant traction given its unique attributes offering regular, defensive income with a focus on security. First mortgage investments are typically short-term, income-focussed investment strategy that can provide investors with stable, passive income via monthly interest payments.

In this blog, we’ll delve into first mortgage investments as an alternative asset class, uncover the mechanics and explain their differences from second mortgages, as well as look into the risks, benefits, and key considerations for discerning investors.

Understanding the mechanisms of first mortgage investments. How do first mortgage investments work?

First mortgage investments entail lending capital directly to borrowers, typically individuals or businesses, in exchange for a first registered mortgage over a specific property or asset which has been offered as the collateral for the loan transaction. This arrangement provides the lender, and the underlying investors, with the highest priority in terms of repayment as the investment is secured by a mortgage over the property. This gives the lender recourse over the property in the event the borrower defaults on the loan. Such investments are commonly employed in real estate transactions, with the property itself serving as collateral. Loan amounts are often determined by the loan-to-value (LVR) ratio, representing the percentage of the property’s value that the loan constitutes.

Because of its lower relative risk, returns for such first mortgage investments are generally lower than investors in the other layers of the capital stack.

Read our blog, 'Understanding the capital stack: A comprehensive guide for all commercial real estate investors', to understand more on how this works.

Differentiating first and second mortgage investments

The primary distinction between first and second mortgage investments lies in their repayment priority in the case of default.

A first mortgage investment takes precedence and is repaid before any other claims on the property.

In contrast, a second mortgage investment holds a subordinate position and is repaid only after the first mortgage has settled – subject to there being residual funds remaining from the sale of the property. Due to the higher risk associated with second mortgages, they generally carry higher interest rates to compensate for their lower priority in default scenarios.

Assessing the risks and benefits of first mortgage investments

First mortgage investments present a compelling opportunity for investors seeking attractive investment returns without a disproportionate increase in risk. First mortgage investments typically offer a regular, monthly income stream via the interest payments with competitive returns to investors who seek capital preservation and capital stability. It can provide investors with exposure to the property market without needing to own the assets. It can provide equity-like returns with the added security via the first mortgage security. However, like any investment, first mortgage investments come with their own set of benefits and risks.

Understanding both sides of the equation is essential for making sound investment decisions.

- Security: First mortgage investments are secured by a primary lien over property collateral, providing recourse and repayment priority for the lender in the event of default.

- Potential for higher returns: First mortgage investments can yield higher returns compared to conventional fixed-income investments or cash/near cash investments like term deposits and high-interest savings accounts.

- Diverse strategies: there are many avenues available to investors wanting to invest in first mortgage investments from single-asset investments to pooled first mortgage investment funds. The underlying security property can also differ greatly and can range – from residential, commercial, industrial, or a combination of all.

First mortgage investments can be a great option to help diversify your portfolio. However, all investments carry risks. Understanding the risks involved is critical before deciding whether a first mortgage investment is right for you and your objectives. Below is a look at the typical risks associated with a first mortgage investment:

- Market fluctuations: Property values can fluctuate, potentially affecting the security property’s value. In the event of a default, there may be shortfalls where the sale proceeds of the security property are not sufficient to recover the invested funds and costs incurred by the lender in enforcing or recovering the repayment of principal and interest under the relevant loan.

- Default risk: If a borrower defaults, there is a risk that an investor may not receive all of their monthly payments, could lose a portion or all of the principal amount they have invested to fund that particular loan and/or could potentially be required to contribute towards any shortfall.

- Investment and liquidity risk: a first mortgage investment is generally considered illiquid in nature. Once you have agreed to invest funds in respect of a particular loan, you are committed to the investment for the full duration of the loan term, which can range from three months to two years, or more. Therefore, once exposed to a loan, your investment is essentially illiquid in nature. You may be unable to convert to cash, the portion of the principal component of a loan you agreed to fund. You must take this into consideration when deciding on what loan types will be suitable for you in light of your overall investment portfolio and needs.

All investments carry risks. Different investment strategies may carry different levels of risk, depending on the assets acquired under the strategy. The risks associated with a first mortgage investment – either as a direct, single-asset investment, directly or via a first mortgage property fund – include possible delays in repayment and a substantial or complete loss of income or principal invested.

A first mortgage investment can offer investors an avenue to diversify their portfolios, benefit from professional management, and gain exposure to the real estate market without the costs associated with direct ownership. The potential for stable income, capital appreciation, and risk mitigation make a first mortgage investment an attractive investment option. However, it is crucial to consider the associated risks and perform due diligence before making any investment decision. You can read further in our Investment FAQs or if you’d like to schedule a call back please click here.

Rising popularity in Australia

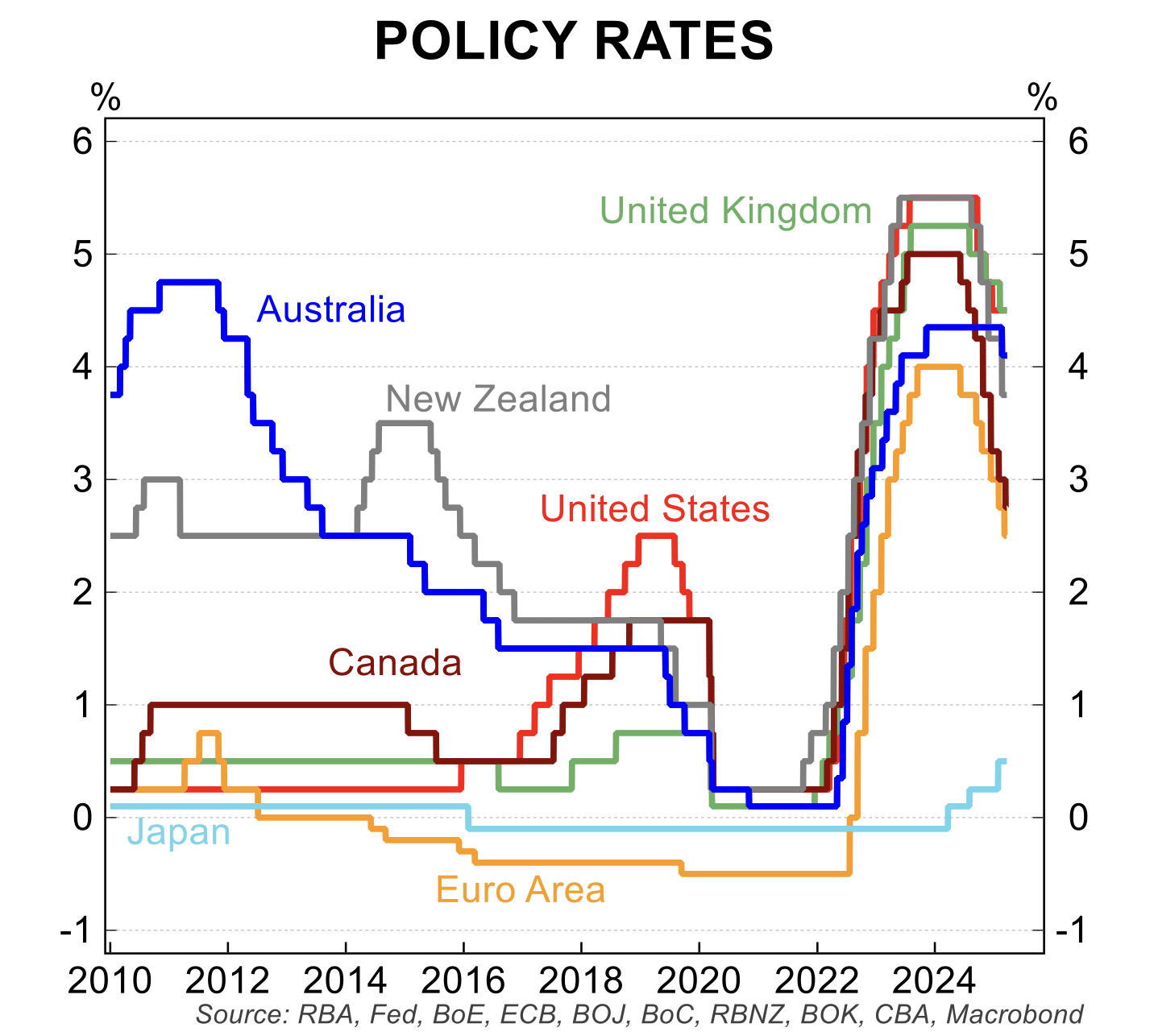

Alternative real estate investments, especially in the form of first mortgage investments, have experienced a surge in popularity in Australia. This alternative asset class provides access to an alternative form of real estate investment without the costs and risks of direct ownership and not only has it proven its ability to ride out periods of rising interest rates but could actually benefit, making it increasingly popular to a growing range of investors.

There aren’t many opportunities for investors to achieve stable, risk-adjusted returns with debt security, but alternative real estate investment managers offer exactly that.

For investors who are attracted to property and real estate investments and the returns it can deliver, but dislike the risk of rising rates and how they might affect it, professionally managed first mortgage investments, especially the commercial real estate debt sector, may be an appealing alternative.

In a rising interest rate environment, first mortgage investments and alternative real estate investments like CRED, have the potential to offer attractive yields but with greater capital preservation, whilst still maintaining exposure to property.

It’s an income-focused investment with a proven ability to ride out periods of rising rates.

With various investment options available, it is crucial to conduct thorough research, seek professional advice, and understand the associated risks.

Get in touch with one of our Investment Directors today to find out more about the first mortgage alternative real estate investments we offer at Zagga.